And Most People Are Still Living Inside Only One Of Them

By Milan Adams

Preppgroup

July 2, 2026

EDITOR'S NOTE:This report is based on a growing body of economic indicators, labor market behavior patterns, and on-the-ground observations across multiple U.S. states. While the official economy continues to show stability on paper, independent data sources and field accounts suggest a rapidly expanding informal labor structure operating outside traditional reporting systems. Readers should be aware that the reality described below reflects a widening gap between measured economic performance and lived financial conditions across large segments of the population.

At 5:03 a.m., in a suburban parking lot outside Atlanta, the day has already begun long before the official economy wakes up. Pickup trucks arrive in silence, parked in uneven rows under flickering streetlights. There are no company logos, no HR onboarding stations, no formal scheduling system displayed on screens or printed notices. Instead, a foreman moves through the crowd with a folded sheet of paper, calling names in a low voice that barely carries through the morning air. Workers respond, step forward, and are assigned to jobs that will never appear in a payroll database. Payment is handled later, in cash, discreetly, with no digital record beyond the work itself.

What is unfolding here is not an exception or a marginal practice. It is increasingly part of a parallel labor structure that has expanded quietly across the United States over the past decade. Construction crews, cleaning teams, delivery work, home repairs, informal logistics, and even digital freelance services now frequently operate through arrangements that sit partially or entirely outside official reporting systems. What was once considered temporary or informal has, in many regions, become a functional layer of economic survival.

The scale of this shift is what makes it difficult to ignore.

The United States remains the largest economy in the world, with GDP exceeding $27 trillion according to recent international estimates. Financial markets continue to set new highs, corporate earnings in key sectors such as technology and healthcare remain strong, and headline unemployment figures suggest relative stability compared to past economic downturns. On the surface, the system appears structurally intact.

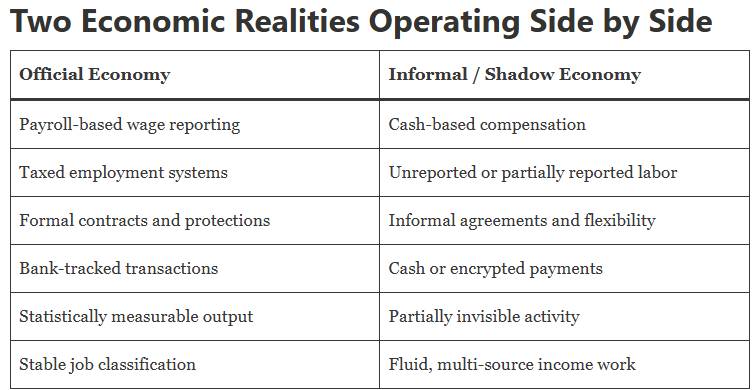

Yet beneath these indicators, another economic layer continues to expand-one that is not fully captured by GDP calculations, labor statistics, or tax reporting systems. Economists typically classify this as the shadow economy, though the term itself understates its complexity. It is not a single market or sector, but rather a dispersed network of informal activity, ranging from cash labor and unreported freelance work to partially concealed small business operations.

In the United States, conservative estimates place this shadow economy at approximately 5% to 7% of GDP, or roughly $1.2 to $1.8 trillion annually, depending on methodology. These figures are inherently imprecise, not due to lack of data collection, but because the very nature of informal economic activity resists complete measurement.

What matters more than its exact size is its trajectory.

Over the past decade, structural economic pressures have steadily pushed more activity outside formal systems. Housing costs have increased at a pace that has consistently outstripped wage growth in many urban and suburban regions. In several major metropolitan areas, rent alone now consumes 30% to 40% or more of household income, leaving limited financial flexibility for savings or unexpected expenses. At the same time, healthcare costs, insurance premiums, transportation expenses, and basic consumer goods have all increased in ways that are not always reflected proportionally in headline inflation metrics.

Even when inflation slows, prices rarely reverse. They stabilize at a higher baseline, creating what economists sometimes describe as "ratchet effects" in cost structures. Over time, this produces cumulative financial pressure rather than temporary strain.

As that pressure builds, households begin to adapt.

This division is not absolute. In practice, the boundary between the two systems is increasingly porous. Individuals often move between formal employment and informal income streams depending on necessity. A worker may hold a traditional full-time job while supplementing income through cash-based weekend work. A small business may operate formally while paying certain labor costs informally. A freelancer may report part of their income while leaving other transactions outside official systems.

The result is not a replacement of one economy by another, but a gradual blending of both.

One of the clearest indicators of this shift appears in household financial behavior. Credit card debt in the United States has surpassed $1 trillion, reflecting sustained reliance on borrowing to maintain consumption levels. Savings rates, meanwhile, have shown volatility, often declining during periods of economic stress when real wages fail to keep pace with living costs.

At the same time, the Internal Revenue Service continues to estimate a tax gap measured in hundreds of billions of dollars annually, representing the difference between taxes owed and taxes actually collected. While this gap is not exclusively the result of informal labor, it reflects broader patterns of underreporting, noncompliance, and structural complexity in income tracking.

Taken together, these indicators suggest not a collapse, but a system under continuous adjustment.

A Pattern Repeated Across the Country

In a midwestern city, a man in his early fifties begins his day at a warehouse loading trucks under a formal employment contract. His paycheck is reported, taxed, and tracked. Yet his actual financial stability depends on what happens after his shift ends. Three evenings a week, he repairs household appliances for cash. On weekends, he works construction jobs arranged through personal contacts. None of this additional income appears in official records, not because of deliberate evasion, but because his primary income no longer covers his monthly obligations.

This pattern is increasingly common across professions that once represented middle-class stability. Teachers supplementing income through tutoring or freelance work. Nurses providing private care services. Electricians and plumbers taking unregistered residential jobs. Delivery drivers combining platform-based gig work with direct, informal arrangements.

The structure of employment has evolved faster than the structure of financial security.

Technological change has accelerated this transformation. Digital platforms now allow services to be advertised, negotiated, and paid within minutes. Peer-to-peer payment systems reduce friction in transactions. Messaging applications coordinate labor informally across local networks. As a result, economic activity that once required formal intermediaries can now occur directly between individuals with minimal oversight.

At the same time, labor markets have shifted toward greater flexibility and reduced long-term security. The growth of contract work, freelance arrangements, and gig-based employment has increased adaptability but also transferred financial risk from institutions to individuals. Workers increasingly manage multiple income streams simultaneously, rather than relying on a single employer.

This fragmentation produces a labor environment where income stability is no longer guaranteed by employment status alone.

Key Structural Indicators

| Indicator | Current Trend |

| Shadow economy size | ~5-7% of GDP |

| Credit card debt | Above $1 trillion |

| Wage vs rent growth | Rent significantly outpacing wages |

| Federal tax gap | Hundreds of billions annually |

| Gig/informal labor share | Gradually increasing |

| Household financial stress | Broad-based rise |

None of these indicators individually suggests systemic failure. However, collectively they describe an economy that is continuously adapting under sustained financial pressure rather than operating in equilibrium.

What distinguishes the current period from earlier phases of American economic history is not crisis, but normalization. Informal income is no longer confined to the margins of the economy. It has become embedded within mainstream financial survival strategies. For many households, it is not considered "extra" income in a discretionary sense, but necessary income required to bridge the gap between wages and cost of living.

Large and small businesses alike have also adjusted. Some rely more heavily on subcontracting arrangements. Others restructure labor relationships to reduce fixed obligations. Smaller firms, facing rising operational costs, sometimes incorporate informal labor practices as a way of maintaining competitiveness. These adaptations are typically pragmatic rather than ideological, driven by cost structures rather than intent.

Over time, these micro-level adjustments accumulate into macroeconomic change.

The result is a system in which two economic realities operate simultaneously. One is visible, measured, and formally recorded. The other is adaptive, partially invisible, and embedded in daily financial behavior across millions of households. One is reflected in official statistics and policy frameworks. The other is reflected in cash transactions, informal labor, and untracked digital exchanges occurring continuously across the country.

Most individuals do not consciously choose between these systems. They operate within both, depending on necessity and circumstance.

And it is precisely this fluid movement between formal and informal activity that defines the current transformation of the American economy more than any single statistic or headline.

Conclusion: The Economy That Changed Without Announcing It

The most persistent misconception about the American economy is the assumption that it functions as a single, unified system that can be fully captured through official data. In reality, it is increasingly composed of two overlapping structures operating in parallel—one visible and measured, the other adaptive and partially unrecorded.

For now, this dual structure maintains balance. It allows households to remain financially active, enables businesses to adjust to cost pressures, and sustains consumption even when formal wages fall short of rising living expenses. But it also signals a deeper transformation: a widening gap between official economic representation and lived financial reality.

What is becoming clear is not a sudden breakdown, but a gradual divergence. The economy has not stopped functioning—it has reorganized itself in ways that traditional models struggle to fully describe.

And this shift did not arrive through policy or announcement. It emerged quietly, in early morning parking lots, in second jobs taken after full shifts, in weekend cash work, and in everyday financial decisions shaped by necessity rather than preference.

Over time, without a defined starting point, a parallel system did not replace the old one—it grew inside it, until both became impossible to separate completely.